Legal Aspects for Online Transactions

Introduction

Online trade transaction, or in its current and commonly-used term, e-commerce, broadly refers to commercial activity conducted with the aid of electronic devices. E-commerce generally refers to electronic business transactions or trades which are wholly or partially conducted over the internet.[1] As e-commerce grows and becomes a more viable and, to a certain extent, safer medium of shopping/trading, it is an industry that requires a strong regulatory framework in order to ensure, among others, accountability and consumer protection. This article intends to explore the legislative framework surrounding e-commerce in Malaysia and the extent to which it regulates online businesses and protects consumers’ interests.

The role of the Ministry of Domestic Trade and Consumer Affairs (“MDTCA”)

MDTCA plays a significant role in regulating online businesses. Just like traditional businesses, online businesses are required to register themselves with the Companies Commission of Malaysia (“SSM”), an organisation that falls within the purview of MDTCA. Via SSM, MDTCA introduced the SSM BizTrust, a standard that can be obtained by online business, which certifies that it has complied with SSM BizTrust’s principles and criteria, e.g. registration with SSM, online security and protection of information represented by logo or seal of assurance displayable on the e-commerce platform and linked to SSM’s report and other relevant information[2] pertaining to the online business which are accessible to the public.

Recently, MDTCA has collaborated with Lazada Malaysia, one of Malaysia’s biggest e-commerce platforms, and the Malaysia Digital Economy Corporation to support local small and medium enterprises and their products on Lazada Malaysia’s website as an initiative to stimulate the nation’s digital-led economic recovery through campaigns such as ‘Buy Malaysia’ and ‘Penjana Shop Malaysia Online.’[3]

When it comes to foreign participation, this is regulated by MDTCA’s Domestic Trade Division, who acts in line with the Guidelines for Foreign Participation in Distributive Trade Services in Malaysia (Amendment) 2020. These guidelines are intended to:-[4]

• ensure an orderly and fair development in the wholesale and retail

industries, while ensuring the growth of local businesses;

• encourage the modernization and increase the efficiency of the industry and its continued contribution to the growth of the economy; and

• increase Bumiputera and Malay participation in the economic sector, in line with the National Development Policy.[5]

Relevant Laws

The relevant laws governing e-commerce transactions in Malaysia are:

• Electronic Commerce Act 2006 (“ECA 2006”);

• Consumer Protection Act 1999 (“CPA 1999”) – the primary legislation on consumer protection in commercial activities including e-commerce;

• Consumer Protection (Electronic Trade Transactions) Regulations 2012 (“CP Regulations 2012”) – regulations issued pursuant to the CPA 1999, which prescribes a set of requirements to be adhered to and complied with by e-commerce traders;

• Contracts Act 1950 (“CA 1950”), which governs contracts in Malaysia; and

• Sale of Goods Act 1957, which governs the sale of goods in Malaysia.

E-commerce is also subject to other legislations, including:

Computer Crime Act 1997;

• Digital Signature Act 1997 (“DSA 1997”), which regulates the use of digital signatures;

• Personal Data Protection Act 2010, which protects data and information collected from consumers by traders from unauthorised use, i.e. without the consumers’ consent;

• Trade Description Act 2011, which deals with, amongst others, advertisements;

• Price Control and Anti-Profiteering Act 2011, which generally deals with price display and product labelling; and

• Weights & Measures Act 1972, which deals with weighting and measuring processes.

There are legislations which are indirectly relevant to e-commerce, such as:

• Registration of Businesses Act 1956 (“ROBA 1956”), which deals with registration of businesses including online businesses;

• Companies Act 2016 (“CA 2016”), which deals with the incorporation and registration of companies carrying on businesses in Malaysia, including online businesses;

• Financial Services Act 2013 and Islamic Financial Services Act 2013, which recognise electronic money as a payment instrument;

• Direct Sales and Anti-Pyramid Scheme Act 1993, which recognises sales through electronic transaction as a form of legal direct sales; and

• Anti-Money Laundering, Anti- Terrorism Financing and Proceeds of Unlawful Activities Act 2001 to which the issuance of electronic money shall be subjected.

It shall also be noted that online businesses with any foreign involvement must comply with the CP Regulations 2012, Guidelines for Foreign Participation in the Distributive Trade Services in Malaysia and all other existing laws and regulations in Malaysia as applicable to physical businesses.[6]

Registration of Online Business

a) Trader who is a Malaysian Citizen or Permanent Resident of Malaysia

On 29 May 2017, YBhg. Datuk Zahrah Abd Wahab Fenner, the then Chief Executive Officer of SSM stated that:

“All online traders who carry out businesses via marketplace or e-commerce companies must register with SSM by end of December2017. SSM will give a 30-day period for the traders to register after their businesses on the e-commerce platform become profitable. Traders who fail to register their businesses will be dropped from the online platform. Actions will be also taken under the Registration of Businesses Act 1956 on traders who did not register and if convicted, may face a two-year jail term or fine of RM50,000, or both.”

Pursuant to Section 5 of ROBA 1956, all businesses shall be registered with SSM. ‘Business,’ for the purpose of ROBA 1956, is inclusive of all forms of trade, commerce, craftsmanship, calling, profession, or other activity carried on for the purposes of gain, but is exclusive of any office or employment or any charitable undertaking or any occupation specified therein.[8] Further, under the Guidelines for Registration of New Business, a set of guidelines issued by SSM which further explains the scope and application of ROBA 1956, businesses that needs to be registered with SSM must be operating in Malaysia and must be owned by Malaysian citizen or permanent resident of Malaysia.

Hence, it is safe to say that any trader, who is either a Malaysian citizen or permanent resident of Malaysia, carrying on online business in Malaysia has to register his/her business with SSM, failure of which[9] the trader commits an offence and, upon conviction, shall be liable to a fine not exceeding RM50,000 or imprisonment for a term not exceeding two (2) years or both.

b) Trader who is a Foreign Citizen (not being Permanent Resident of Malaysia)

Online businesses in Malaysia operated by foreign citizens (not being permanent resident of Malaysia) are not required to be registered with SSM but it shall be established via company incorporation or company registration. [10] To clarify, the foreign citizen trader, in order to establish online business in Malaysia, needs to incorporate a company or, if the trader already has a foreign company incorporated under the relevant foreign law, to register the foreign company, under the CA 2016[11].

What about Online Businesses operating from Outside of Malaysia?

One of the pressing issues that have been lingering for the past few years concerning cross-border e-commerce since the formal enforcement on registration of local online businesses with SSM is whether online businesses operating from outside of Malaysia should be subjected to the same registration requirement;[12] if not, there remains an open opportunity for cross-border online businesses to take the lion’s shares in transacting with the local consumers as they would not be consequently subjected to the requirements of Malaysian laws suchas requirement for licences especially considering that some of the local traders are still reluctant to have their respective online businesses registered with SSM amid the formal enforcement executed by SSM.

All is to suggest that the playing field must be level in particular for local small and medium enterprises where resources and funding options are limited, without abandoning the government’s practical policy in allowing and attracting foreign investment into Malaysian markets generally and e-commerce market specifically. Currently, it seems that the business policies adopted by the government are quite relaxed and welcoming where cross-border online businesses can be carried on in Malaysia without the need to establish a local company for that purpose[13].

Tax Aspect of E-Commerce Transactions

a) Income Tax

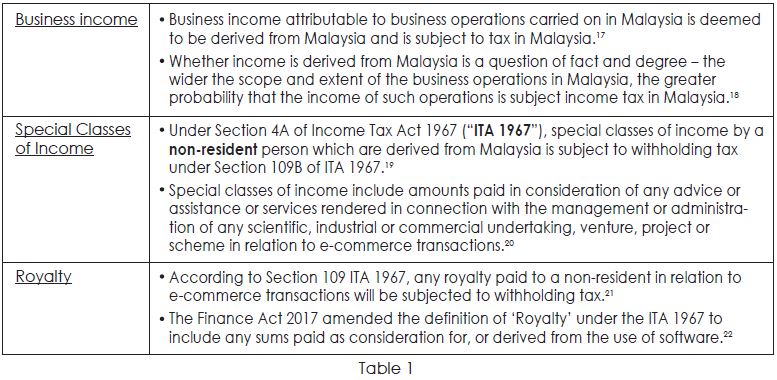

In 2019, the Inland Revenue Board of Malaysia (IRB) issued the Guidelines on Taxation of Electronic Commerce Transactions[14] (“E-Commerce Taxation Guidelines”) which seeks to provide guidance on the income tax treatment with regards to e-commerce transactions.

According to the E-Commerce Taxation Guidelines, the IRB adopts the principle of neutrality whereby both e-commerce transactions and conventional transactions are subject to the same tax treatment.[15] Income is deemed to be derived from Malaysia if it is associated to any activities in Malaysia, regardless of whether that income is received in Malaysia or otherwise.[16] The E-Commerce Taxation Guidelines summarised the tax liability in relation to e-commerce as follows: (Refer TABLE 1)

b) Service Tax on Digital Services

Malaysia recently introduced a new tax regime in relation to digital services – effective 1 January 2020, digital services provided by registered foreign service providers to Malaysian consumers will be subject to a 6% service tax. Foreign service providers (“FSPs”) with a total value of digital services exceeding RM500,000 for a period of twelve (12) months or less are required to be registered.[23] The registered FSP must collect the service tax on the provision of digital service and remit the same to the Royal Malaysian Customs Department.[24]

Digital service is defined as “any service that is delivered or subscribed over the internet or other electronic network and which cannot be obtained without the use of information technology and where the delivery of the service is essentially automated.” [25]

FSP is defined as :[26]

• any person who is outside Malaysia providing any digital service to a consumer;

• includes any person who is outside Malaysia operating an online platform for buying and selling goods or providing services (whether or not such person provides any digital service); and

• who makes transactions for provision of digital services on behalf of

any person.”

Examples of FSP that have registered include Spotify, Netflix and Airbnb.[27] However, where a company who is a foreign registered person (i.e. a FSP that is registered under the Service Tax Act 2018) provides any digital service to any company in Malaysia within the same group of companies with the foreign registered person, such digital service is not subject to service tax.[28]

Legality and Scope of E-Commerce

E-commerce is a valid and legally recognised medium of trade transactions vide the ECA 2006. Pursuant to Section 7 of the ECA 2006, a contract formed (in accordance with the CA 1950) through electronic communication is valid, binding and enforceable by and on the contracting parties. For this purpose, Section 9 of the same legislation recognises electronic signature i.e. signature executed via electronic means in accordance therewith, including digital signature framed pursuant to the requirements under the DSA 1997.

The CP Regulations 2012 governs two (2) groups of persons: (i) e-commerce traders (who are doing business through personal websites and/or websites provided and maintained by e-commerce market operators) and (ii) e-commerce market operators (who provide websites for e-commerce traders such as Mudah.my, Lazada and Shopee) with their respective obligations as follows: (Refer TABLE 2)

Any person who commits an offence under the CP Regulations 2012 shall be liable, upon conviction, to the following:[29] (Refer TABLE 3)

Conclusion

As e-commerce is still developing, the legislations already in place are still not comprehensive and require further development to suit and cater to the needs of the market and its participants at the material time. Perhaps, in addition to amending the existing legislations to solidify and modernise the same, new legislations may be enacted to further strengthen the current set of legislations contemporaneous with the development and expansion of e-commerce in Malaysia. In the foreseeable future, it is envisaged that e-commerce will become an equally popular (if not more popular) alternative to face-to-face trade transactions for the consumers to do their shopping and for the traders to conduct their businesses, due to its practicality, convenience and accessibility.

——————–

1 See https://www.miti.gov.my/index.php/glossary/term/228

2 See https://biztrust.ssm.com.my/iw/about-biztrust

3 The Edge Markets, “Lazada features two new online campaigns to support local businesses”<https://www.theedgemarkets.com/article/lazada-features-twonew-online-campaigns-support-local-businesses>

4 Paragraph 2.0 of the Guidelines for Foreign Participation in Distributive Trade Services in Malaysia

5 Ibid.

6 See https://www.kpdnhep.gov.my/en/component/content/article/14-perdagangan/perniagaan/perdagangan-pengedaran/58-distributive-trade.

7 See https://www.smeinfo.com.my/starting-yourbusiness/going-online

8 Section 2 of ROBA 1956

9 Section 12(1) of ROBA 1956

10 See https://www.mida.gov.my/home/starting-upbusiness/posts/

11 See https://www.tmogroup.asia/ecommerce-inmalaysia-how-to-begin/

12 The Star, “Online businesses have six months to register and pay taxes”< https://www.thestar.com.my/opinion/letters/2017/06/06/online-businesses-havesix-months-to-register-and-pay-tax>

13 See https://www.tmogroup.asia/malaysia-crossborder-ecommerce-insights-and-analysis/

14 Inland Revenue Board Malaysia, Guideline on Taxation of Electronic Commerce Transactions <https://lampiran2.hasil.gov.my/pdf/pdfam/guidelines_e_commerce_13052019.pdf> (Accessed on 10 August 2020)

15 Paragraph 1.3 of the E-Commerce Taxation Guidelines

16 Paragraph 4.2 of the E-Commerce Taxation Guidelines

17 Paragraph 5.1 of the E-Commerce Taxation Guidelines

18 Ibid.

19 Paragraph 6.1 of the E-Commerce Taxation Guidelines

20 Paragraph 6.2 of the E-Commerce Taxation Guidelines

21 Paragraph 7.1 of the E-Commerce Taxation Guidelines

22 Paragraph 7.2 of the E-Commerce Taxation Guidelines

23 Royal Malaysia Customs Department, Guide on: Digital Services by Foreign Service Provider (FSP)

24 Ibid.

25 Section 2 of the Service Tax Act 2018

26 Ibid.

27 The Star, “6% tax on service from Google, FB, Airbnb to take effect Jan 1” <https://www.thestar.com.my/news/nation/2019/12/30/msians-can-expect-pricehikes> (Accessed 11 August 2020)

28 Service Tax (Digital Service) Regulations 2019

29 Section 145 of the Consumer Protection Act 1999 (Act 599)

Written by:

Mohammad Ashraf Mohamed Sopiee (Partner) ashraf.sopiee@azmilaw.com

Shamimi Saberi & Shazana Abd Hapiz (general@azmilaw.com)